Phosphorus , symbol P and atomic number 15 ,is a nonmetallic chemical element. phosphorus as a mineral is almost always present in its maximally oxidised state, as inorganic phosphate rocks.

Types-

Phosphorus derivatives- Types-

- White phosphorus

- Red phosphorus

- Industrial phosphates (sodium, calcium, potassium, aluminum, and magnesium phosphates)

- Phosphoric acid

- Phosphorus chlorides

- Phosphorus pentasulfied

- Phosphorus pentoxide

Applications-

Red Phosphorus (Source-Google images)

White Phosphorus (Source-Google images)

Phosphorus fertilizers,as basic nutrient for plant growth also serves for higher and faster yields of crops. This has made fertilizers the most

important application of phosphorus and its derivatives market.

Fertilizers also finds applications in detergents of phosphorus and its

derivatives. Government bodies of developed countries have imposed

regulations on the use of phosphorus in detergents that restricts the

growth in the developing countries.Phosphorus forms a number of derivatives, of which ammonium phosphates

has the highest market share. Its use in fertilizers has been driving

its demand.

Red Phosphorus (Source-Google images)

White Phosphorus (Source-Google images)

Yellow phosphorus is an intermediate in the

production of phosphorus derivatives. Its production is highly energy

intensive with electricity playing a major role in the cost of

production. The major countries that produce yellow phosphorus are

China, U.S., Kazakhastan, and Vietnam.

Major players in this market are OCP Sa (Morocco),

The Mosaic Company (U.S.), PotashCorp (Canada), EuroChem (Russia),

PhosAgro (Russa), Vale S.A. (Brazil), Isreal Chemicals Limited (Isreal),

Prayon group (Belgium), Innophos Holding Inc. (U.S.) and United

Phosphorus Limited (India). A number of Chinese players such as

Yuntianhua Group Co. Ltd, Jiangyin Chengxing Industrial Group Co. Ltd,

and Hubei Xingfa Chemicals Group Co. Ltd operate in this market.

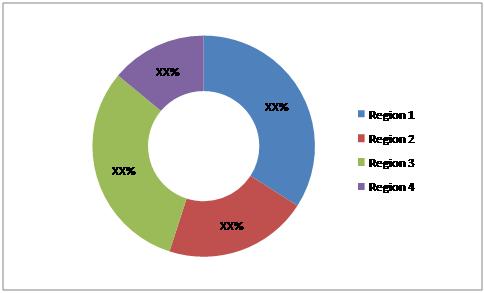

Phosphorus & Its Derivatives Market Share, By Geography, 2012

Source: MarketsandMarkets Analysis

Asia has been identified as the largest market as

well as the highest growing in the next five years among all regional

markets. Asia has emerged as an important consumer with China being the

largest producer and consumer while India accounts for the largest

imports of phosphorus and its derivatives. The need to be self

sufficient in meeting domestic food demands has been driving the

consumption of phosphorus in terms of fertilizers and crop protection

chemicals. The other regions covered are Americas (constituting North

America and South America), Europe, Africa, Oceania and the Middle East.

For more information,visit-